Quarterly Market Review: Q3 2022

By: Paul Dickson, Director of Research and Mark Stevens, Chief Investment Officer

How much are recession expectations already priced in?

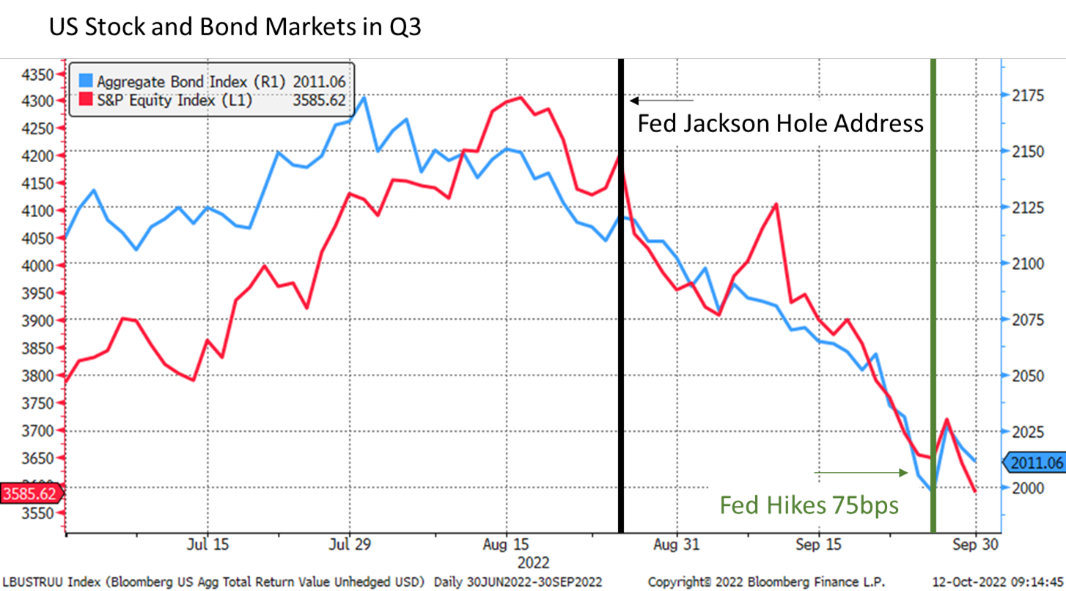

The third quarter of 2022 will be remembered as the turning point in the battle against inflation. Global central banks, led by the U.S. Federal Reserve, appeared to decide that risking a recession would be preferable to risking rising inflation, and the markets took heed. U.S. equity markets started the quarter by recovering from earlier declines. This recovery was quickly upended by the Fed’s unsettlingly sharp interest rate increases and an extraordinary hawkish turn in policymaker rhetoric.

With inflation figures remaining stubbornly high and labor markets showing no slack, the Federal Reserve doubled their policy rate – raising the overnight “Fed Funds” rate from 1.5% to 3.0%. This signaled for several additional rate hikes over the coming months, making it the most rapid pace of monetary tightening since the early 1980s. The reaction has been a sharp decline in both stocks and bonds, which raises the question: How high is the risk of an appreciable recession over the coming months, and how much is already priced in financial markets?

The Hangover: Cure feels worse than the condition

At the start of 2022, we presented the argument for the year of “shifting gears.” Rescuing the economy from the sudden shock of the pandemic shutdown relied on extraordinary fiscal and monetary efforts. We are now seeing these effects reversed in an equally remarkable manner. There is an old saying that the job of the Central Bank is to know when to take away the punchbowl (of lower than appropriate interest rates given the state of the economy) just when the party is warming up. To take the metaphor one step further: the party went too long and with an ever-full punchbowl, inflation is the resulting hangover.

At the end of last year, the Federal Reserve assured the markets that the rising levels of inflation would prove to be transitory. They believed that the Fed Funds rate at the end of 2022 would be under 1% and never exceed 3% out as far as their forecasts allowed. In hindsight, the Fed was clearly wrong at the time. As it became apparent that the rise in prices threatened to become endemic and entrenched in public expectations, the Fed started its tightening cycle, albeit late.

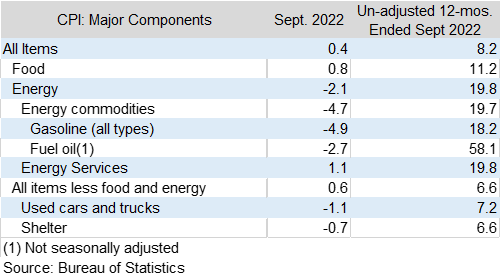

The latest inflation figures have continued to pressure the markets. The Consumer Price Index rose 0.4% in September, greatly exceeding expectations of a 0.2% rise. This brings the year-on-year figure to 8.2%, a 40 year high. This almost assures a 75bps rate hike on November 2 and increases the probability that the Fed could hike even further at that meeting. As it stands, there is likely more than 100bps of additional rate hikes through the end of the year.

But there is some good news in the inflation report. Energy costs continue to fall, and as a component of many other sectors, this should have some additional impact. The famous supply chain bottlenecks in the auto industry and the run up in used car and truck prices have ebbed enough to allow that sector to see price declines. Shelter remains a concern as the year-on-year increase of 6.6% remains very high.

One complication for the shelter statistic is that it is calculated using actual rents and an owner-equivalent rent figure. These notoriously did not capture the house price mania in the early aughts and may lag the decline in house prices we are witnessing now. Another complication is that actual rents typically lag since leases are usually locked in for some time. But as of this writing, it is too early to know if the recent declines in house prices will be reflected quickly in the data.

Shelter Slump Has Started and Could Be Key

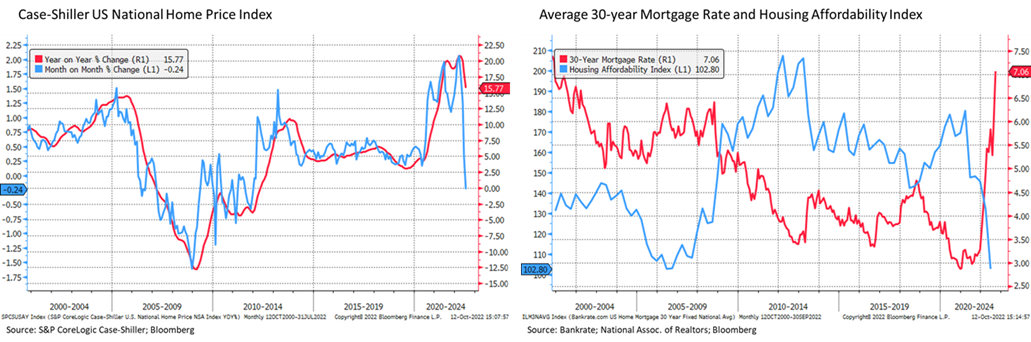

As mentioned, shelter comprises approximately one-third of most price indices. Higher interest rates directly impact the financing of everything in the economy, especially housing. Last year the average 30-year fixed mortgage rate hit a low of 2.8% but has since risen to over 7.0%. This has led to a steep decline in housing affordability according to the National Association of Realtors. It is likely the primary cause of signs that the tremendous appreciation in house prices has started to wane. The latest reading of national home prices in July showed a monthly decline of 0.24%, the first in a decade, bringing the year-on-year number down to 15.7% from over 20% as recently as April.

Labor Market Shows Limited Softening

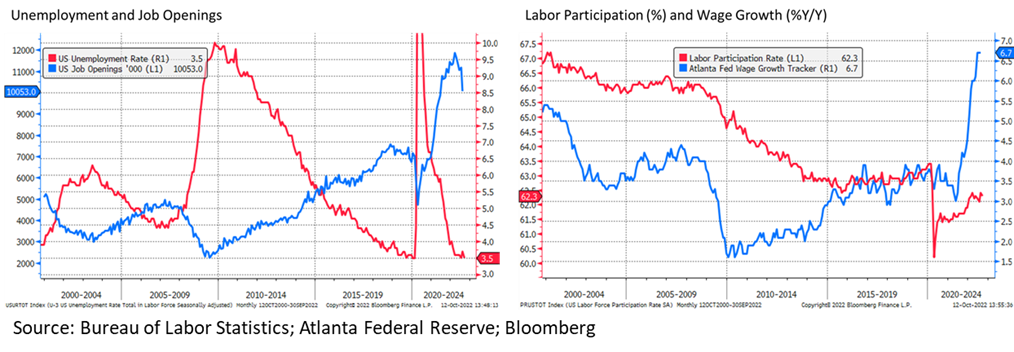

As much as shelter drives the actual inflation data, the Fed appears more concerned with the outlook for unemployment and wages. Labor costs do not directly appear in the inflation statistics, but are considered a key driver of inflation because rising prices have historically led to higher wages. This cycle provides headroom for more inflation leading to more wage growth. The famous NAIRU (Non-Accelerating Inflation Rate of Unemployment) concept guided policy makers in decades past. It assumed that there was some lower bound of unemployment at which inflation would be bid up through rising wages. That relationship seemed to have been disrupted through globalization, the decline in unionization, and other gains in productivity (automation), but now seems to weigh more heavily on policymakers’ minds. The labor market has remained very tight, wages have been rising substantially and Fed officials openly opine that an increase in unemployment might be a necessary outcome from efforts to bring inflation down. Unless labor participation rises significantly, a recession is the most direct way to soften the labor market.

The most recent labor data has, on balance, continued to be strong thus raising the likelihood of additional rate hikes. The one silver lining in the most recent numbers was decline in job openings by one million. The overall figure remains worrisomely high at 10 million, which represents nearly two open jobs for every unemployed person. That has helped fuel the rapid rise in wage compensation as tracked by the Atlanta Federal Reserve.

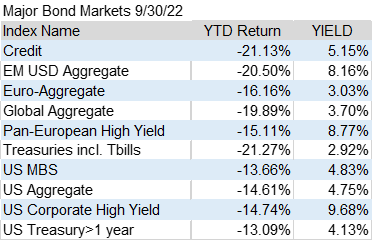

Worst Bond Market in Memory Revives Interest in Bonds.

Rising interest rates translate to falling bond prices, and this year has seen the worst performing bond market since the 1960s. Bonds are usually a safe haven from declines in the stock market; interest rates typically fall during bad economic news, leading to bond price gains. This year the relationship has reversed. The rise in interest rates is the leading cause of equity declines as tightening monetary policy to rein in inflation threatens the economic outlook.

This year has been a shock to investors that are used to the safety of the bond market. Total returns for diversified fixed income categories that traditionally serve as ballast in core portfolios were negative for the third consecutive quarter, with most strategies down by double-digits year-to-date. The U.S. Intermediate Aggregate Index declined 3.8% and is now down 11.0% for the first nine months of 2022. The Barclays Municipal Bond Index had similar returns of -3.5% and -12.1%.

Higher yields have made the bond market a more interesting investment opportunity than it has been in recent years. Pundits are already saying that the 60/40 portfolio is back as a realistic strategy to manage investments. There are likely to be some headwinds to bond markets as monetary authorities remain poised to raise interest rates further. But just like the repricing in equities, much of the damage has been done already. Putting cash to work in bonds now, or waiting just a short time, seems to be a prudent course of action.

It is important to note that the U.S. Treasury Yield Curve is inverted, which is a classic sign that a recession is looming. Bond investors are betting that the rate hike cycle is nearing completion and as it may cause a recession -- or at least a significant slowdown -- and a decline in inflation then interest rates in the future will be lower than they are now. Rather than miss the price appreciation when that occurs, investors are now putting money to work in longer securities now on the belief rates are destined to fall again over the medium term.

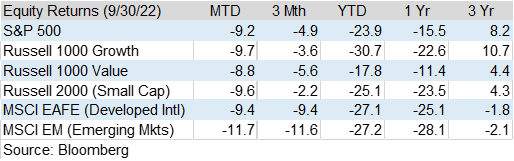

Equity Markets Repriced Again

The S&P 500 gained 9.2% in July, only to give way to further selling following the hawkish comments by Fed Chairman Powell. By the end of September, the market had hit new lows, ending Q3 with a -4.9% return, and pushing the S&P 500 back into bear market territory (-23.9% year-to-date).

Growth stocks (-3.6%) were also down in Q3, but managed to beat Value stocks (-5.6%) for the first time in nearly a year. Growth outperformance mostly took place in the July market advance and subsequently gave way to Value later in the quarter. Since the market peak on August 16, Value outperformed Growth by over 8%. Small Cap stocks (-2.2%) turned in the best relative performance among domestic equities in Q3.

The surge in interest rates helped the U.S. Dollar Index soar, gaining 17.2% year-to-date. For U.S. investors, a strong currency hurts international performance when converted back to U.S. dollars. The MSCI EAFE Index (-9.4%) and Emerging Markets (-11.6%) under-performance relative to the U.S. stocks has been due, at least in part, to dollar strength not seen in many years.

Markets Likely Pricing in a Shallow Recession

Investors face a new cycle: one where the Fed is unwinding much of the excess, inflation is stubbornly high, and the productivity (and costs savings) brought by globalization is fading. This potentially makes stock market recoveries longer and likely paired with greater volatility.

As interest rates rise, the risk of a recession increases. Whether it will be deep or shallow remains to be seen, but given the pace of rate hikes and the need for softer labor and housing markets, a recession over the coming year seems likely. Since the banking system is well capitalized, it won’t be a replay of the Great Recession, during which the functioning of the economy was impaired. Rather, it will be concentrated in those sectors that thrived due to the low interest rate policies of recent years but now are unattractive in a more normalized environment. The steep decline in crypto currencies and the near collapse of the NFT (non-fungible token) market are examples where pure speculation cannot compete against safer alternatives when the latter provides reasonable returns. This is also now evident within the sub-investment grade loan market where there have been significant write-offs and the issuance of new securities has dried up.

S&P 500 earnings estimates for 2022 and 2023 are roughly $223 and $240 per share according to FactSet Research. Higher input costs, wage pressures, and ongoing supply chain shortages could put pressure on profit margins. Q3 earnings results will provide key insights into the magnitude of margin pressures and overall earnings visibility. Have valuations come down enough to reflect weaker earnings prospects? The S&P 500 has declined so much that the forward price/earnings ratio (15.5x) has now fallen below the 25 year average.A decline of 10% in 2022 earnings would put the P/E multiple just shy of 18x. This is not overly expensive, but would likely give the markets a fair amount of indigestion in the short run.

Opportunities Exist Even if Market Bottom Remains Illusive

We continue to see opportunities in Value stocks compared to Growth stocks. Valuations are more attractive and Value stocks are less sensitive to rising interest rates. Their outperformance has been significant year-to-date, and after a decade of underperformance, we believe there is still room to outperform. Low-volatility stocks have similar traits to Value. They often exhibit higher quality, and have historically outperformed in down markets. Hedged equity and other alternative investments provide some downside protection and provide a less-correlated return stream compared to equities and bonds.

Higher yields on short-term treasury, corporate, and municipal bonds mean improving high-quality fixed income return opportunities. With Treasury yields over 4.0% across most of the yield curve, bonds now look more attractive, and play a larger role in a diversified portfolio. Short-term bonds can help investors mitigate losses due to rising rates since their prices fluctuate less when yields change.

Discuss taking losses (in taxable accounts) if you have them with your tax advisor. There are few benefits in losing money. One consolation prize is the ability to offset investment losses against capital gains and/or income. Even if you don’t have gains this tax year, losses generally can be carried forward to offset future gains/income. Strategic tax loss harvesting throughout the year can be an attractive strategy to maximize after-tax returns.

Eliminate concentrated positions or underperforming investments. Use the opportunity to improve the quality of your portfolio and diversify across other asset classes. Many asset classes have underperformed Large Cap U.S. equities and represent attractive risk-adjusted returns in the new investment cycle.

We have noted many of the economic signs point to slowing and inflation may very well have peaked. Additionally, economists estimate that losses from financial markets (and home prices) could exceed $10 trillion – representing a huge drag on consumer demand not accounted for in current data. Why is peak inflation important? According to Blackrock, since 1927 the average S&P 500 return in the 12 months following a top in inflation is 11.5%. We believe that the biggest risk of it not happening this time is that the Fed overshoots and forces the economy into a deeper recession than the market is already pricing in.

Wealth Management does not provide accounting, legal or tax advice. This information discusses general economic and market activity and is presented for informational purposes only and should not be construed as investment advice. Views and opinions expressed herein do not account for any specific investment objective, restrictions, and/or financial circumstances of any specific client. Investors are urged to consult with their financial advisors before buying or selling any securities.

Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. The investment return and principal value of investment securities will fluctuate based on a variety of factors, including, but not limited to, the type of investment, amount and timing of investments, changing market conditions, currency exchange differences, stability of financial and other markets, and diversification. The statements and opinions expressed in this article herein are those of the author as of the date of the article and are subject to change. Content and/or statistical data may be obtained from public sources and/or third-party arrangements and is believed to be reliable as of the date of the article.

Products offered through Wealth Management are not FDIC Insured, are not bank guaranteed and may lose value.